.png)

Statement of Functional Expenses: Guide & Free Template

Statement of Functional Expenses: Nonprofit Guide + Free Template

The statement of functional expenses is a required financial report for nonprofits with gross receipts over $200,000 or assets over $500,000. It shows exactly how much you spend on programs versus administration and fundraising, giving stakeholders a transparent view of where every dollar goes.

This guide explains what a statement of functional expenses is, why it matters, how to prepare one, and how to use it to build trust and make smarter decisions. You'll also find a free template with built-in formulas and a realistic example to help you get started.

If you are just here for the template, grab it here.

Key Takeaways

- Transparent spending breakdown: The statement categorizes expenses by function (program, administrative, fundraising) to show how resources advance your mission.

- Required for compliance: Large nonprofits must include this statement when filing Form 990 with the IRS.

- Builds donor confidence: Clear functional expense reporting demonstrates responsible stewardship and strengthens supporter relationships.

- Guides better budgeting: Comparing actual spending to projections helps you allocate resources more effectively.

- Nonprofit-specific reporting: Unlike for-profit financial statements, this report is designed specifically for mission-driven organizations.

What Is a Statement of Functional Expenses?

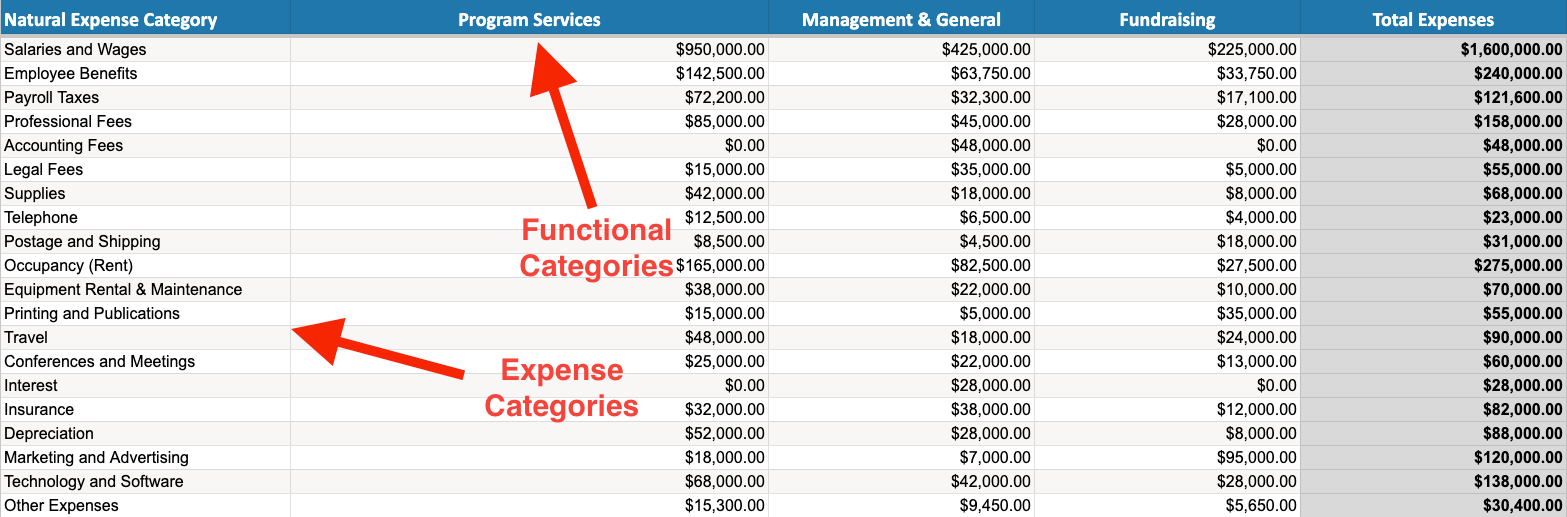

A statement of functional expenses is a financial report that categorizes your nonprofit's costs based on their purpose. It's organized as a matrix or table where:

- Rows list your natural expense categories (the nature of each payment made), such as salaries, rent, supplies, and insurance.

- Columns organize those same expenses by functional category (how the expense supports your mission): program services, management and general, and fundraising.

How It Fits With Other Nonprofit Financial Statements

The statement of functional expenses is one of four essential financial statements that nonprofits prepare annually:

- Statement of Activities (Income Statement): Shows your revenue, expenses, and changes in net assets over a period.

- Statement of Financial Position (Balance Sheet): Provides a snapshot of your assets, liabilities, and net assets at a specific date.

- Statement of Cash Flows: Tracks how money moves in and out through operating, investing, and financing activities.

- Statement of Functional Expenses: Breaks down spending by both natural category and functional purpose.

The first three statements have direct for-profit equivalents: income statement, balance sheet, and cash flow statement.

The statement of functional expenses is unique to nonprofits. It exists specifically to show how your spending furthers your mission.

Why the Statement of Functional Expenses Matters

Tax Filing and Compliance

If your nonprofit files Form 990 (for organizations with gross receipts of $200,000 or more or total assets of $500,000 or more), you're required to complete a statement of functional expenses as part of your filing.

Organizations filing Form 990-EZ, Form 990-PF (for private foundations), and certain state tax forms also include abbreviated expense reporting sections. Your internal functional expense statement becomes the source document for completing these forms accurately.

Transparency and Donor Trust

Donors increasingly want to see how nonprofits allocate resources. The statement of functional expenses provides concrete evidence that contributions are being used responsibly.

When you can show that the majority of spending goes toward programs rather than overhead, you build confidence with:

- Individual donors who want their gifts to make direct impact

- Foundations and grantmakers evaluating your stewardship

- Board members assessing organizational effectiveness

- Community stakeholders holding you accountable

Include a summary or visual from your statement in your annual report, or have the full statement ready when supporters request detailed financial information.

Strategic Budgeting and Planning

By comparing your actual expenses with last year's budget projections, you gain insights that inform smarter resource allocation.

For example, if your after-school program's expenses exceeded projections by 25% while another program came in under budget, you can adjust next year's allocations accordingly. You might also discover opportunities to share resources between programs or identify cost-saving measures in administrative functions.

Internal Decision-Making

The report helps leadership answer critical questions:

- Are we investing enough in program delivery?

- Is our fundraising spending generating adequate return?

- Which programs are cost-effective, and which need more support?

- Can we afford to launch a new initiative?

Using the statement to track trends over multiple years reveals patterns that guide long-term strategy.

The Three Functional Expense Categories

Understanding how to categorize expenses is essential for accurate reporting. In general, every nonprofit expense falls into one of three functional categories:

1. Program Expenses

Program expenses directly support your mission-driven activities. These costs vary widely depending on your organization's focus:

- An animal shelter might include veterinary supplies, pet food, and adoption event costs.

- A literacy nonprofit would report books, tutoring materials, and instructor wages.

- A food bank would include food purchases, warehouse operations, and distribution costs.

The key question: Does this expense directly advance the work we exist to do?

2. Management and General (Administrative) Expenses

These are the costs necessary to operate your organization day to day. They keep the lights on and the organization running smoothly:

- Office rent or mortgage payments

- Utilities and insurance

- Accounting and legal fees

- Administrative staff salaries

- General office supplies and equipment

- Technology infrastructure

3. Fundraising Expenses

These are the upfront costs associated with generating revenue:

- Fundraising software subscriptions

- Event planning and execution

- Marketing and donor communications

- Grant writing services

- Donor stewardship activities

Understanding the "Overhead Ratio"

You may have heard that nonprofits should spend at least 65% on programs and no more than 35% on overhead (administrative + fundraising combined). This was treated as a hard rule for years. Every organization's ideal ratio actually differs based on size, age, and mission.

Startup nonprofits typically show 40-50% overhead in years 1-3, dropping to 30-35% by year 5 as donor acquisition costs stabilize and program infrastructure scales. Mature organizations with established donor bases often achieve 70-80% program spending.

The key is to be transparent about your spending, strategic in your allocations, and always working to maximize mission impact.

Functional Expense Benchmarks by Sector

Your ideal ratio depends heavily on your organization's type and maturity. Here are typical range estimates across nonprofit sectors:

Why the differences? Arts organizations typically invest more in fundraising (galas, events, donor cultivation). Healthcare nonprofits often have lower overhead because they generate significant program service revenue. Social services organizations usually maintain lean operations with most resources going directly to beneficiaries.

Use these benchmarks as guides. They're not mandates. If your ratios fall significantly outside your sector's norm, be prepared to explain why to donors and board members.

If you do need to reduce costs, start with overhead efficiencies before cutting program spending:

- Request in-kind donations for event needs

- Implement energy-saving measures in your facilities

- Negotiate better rates with vendors

- Share administrative resources with partner organizations

How to Prepare a Statement of Functional Expenses

Follow these steps to build your statement:

Step 1: Organize Your Chart of Accounts

Your chart of accounts is the foundation. Make sure your expense accounts are clearly labeled by natural category (salaries, rent, supplies, etc.). If your accounts aren't well organized, start by cleaning up your structure.

Step 2: Gather Expense Data

Pull expense totals for your reporting period (typically a fiscal year). You'll need the total spent on each natural expense category: salaries, benefits, professional fees, occupancy costs, etc.

Step 3: Allocate Expenses by Function

This is the critical step. For each natural expense, determine how much should be attributed to program services, management and general, and fundraising.

Some expenses are straightforward:

- Grant writing consultant fees → 100% Fundraising

- Program supplies for a youth camp → 100% Program

- Accounting fees → 100% Management and General

Others require allocation:

- Executive Director salary → Split based on time allocation (e.g., 40% program, 40% admin, 20% fundraising)

- Rent → Split based on square footage used by each function

- Technology costs → Allocated by user count or system usage

Document your allocation methods clearly. Consistency matters for audit and compliance purposes.

Step 4: Build Your Matrix

Create a table with:

- Natural expense categories in rows

- Functional categories in columns

- Allocated amounts in each cell

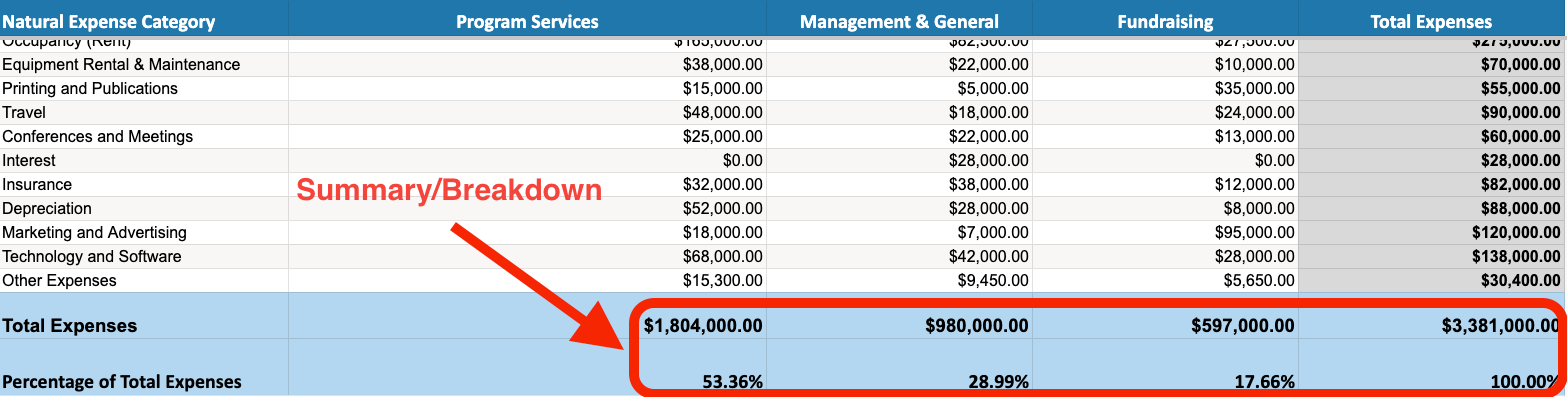

- Totals at the bottom and right side

Step 5: Calculate Percentages

Add a row showing what percentage of total expenses each functional category represents. This gives stakeholders an at-a-glance view of your resource allocation.

Step 6: Use a Template

To make this easier, download our free Statement of Functional Expenses Template

It includes:

- Pre-built structure with common expense categories

- Automatic calculations and totals

- An example with realistic numbers to guide you

The template is available in both Excel and Google Sheets formats.

Tricky Allocation Scenarios and How to Handle Them

In our experience, these gray-area expenses cause the most confusion for nonprofit bookkeepers:

Scenario 1: Executive Director Who Wears All Hats

The Problem: Your ED spends time on program oversight, administrative management, fundraising strategy, and board relations. How do you split their salary?

Recommended Method: Time allocation based on actual time tracking over a representative period (typically one quarter).

Example allocation:

- 35% Program (attending program meetings, program planning, direct program oversight)

- 40% Management & General (HR, finance review, facility management, board governance)

- 25% Fundraising (donor meetings, grant strategy, fundraising events)

Documentation: Keep quarterly time logs or calendar audits. Revisit annually and adjust if role changes significantly.

Scenario 2: Shared Facility Costs

The Problem: Your building houses program activities, administrative offices, and occasional fundraising events. How do you allocate rent, utilities, and maintenance?

Recommended Method: Square footage allocation is most defensible.

Example:

- Measure actual square footage used by each function

- Program space (classroom, service delivery areas): 2,400 sq ft = 60%

- Administrative offices: 1,200 sq ft = 30%

- Multi-purpose space (weighted by usage): 400 sq ft = 10%

Documentation: Create a facility map with measurements and take photos. Update when space usage changes.

Scenario 3: Technology Serving Multiple Functions

The Problem: Your CRM system tracks donors (fundraising), manages program participants (program), and handles vendor payments (admin).

Recommended Method: User count or time-based allocation.

Example allocation for a donor management/program tracking system:

- 50% Fundraising (primary purpose is donor cultivation)

- 30% Program (tracks program participants and outcomes)

- 20% Management & General (generates financial reports)

Documentation: Document the primary use case and percentage of features used for each function. Be consistent year-over-year unless usage genuinely changes.

Statement of Functional Expenses Example

Here's what a completed statement looks like for a midsize regional nonprofit:

This organization demonstrates a healthy balance: the majority of spending goes toward mission delivery, while maintaining adequate investment in operations and fundraising growth.

What Auditors Actually Look For

Having worked with auditors on dozens of nonprofit financial statement reviews, we can tell you exactly what they check when reviewing your statement of functional expenses:

1. Allocation Methodology Documentation

What they want: Written policies explaining how you allocate shared expenses.

Red flags they watch for:

- No documented methodology

- Methodology changed from prior year without explanation

- Allocation percentages that seem arbitrary or too round (all 50/50 splits raise eyebrows)

Pass the test: Create a one-page allocation policy document. Update it annually and have it approved by your board or finance committee.

2. Consistency Year-Over-Year

What they check: Compare current year functional percentages to prior years.

Red flags:

- Program percentage jumped from 65% to 85% with no explanation

- Allocation methods changed without documentation

- Same expense allocated differently in different periods

Pass the test: Run a year-over-year comparison yourself before the audit. Prepare explanations for any significant changes (new program launch, major fundraising campaign, etc.).

3. Reasonableness Tests

What they evaluate: Do the allocations make sense given your organization's activities?

Red flags:

- Organization with major fundraising events showing only 5% fundraising expenses

- New organization showing 90% program expenses (unrealistic for startups)

- Salaries allocated 100% to one function for staff who clearly wear multiple hats

- Facility costs allocated entirely to program when offices clearly exist

Pass the test: Step back and ask "Does this pass the common sense test?" Compare your ratios to sector benchmarks.

4. Joint Cost Allocation Compliance

What they scrutinize: Any expenses allocated between program and fundraising.

Red flags:

- Joint costs allocated without meeting the three-criteria test

- Allocation percentages not supported by content analysis

- No documentation of audience selection criteria

- Materials not retained for review

Pass the test: Keep physical copies of all materials. Document your three-criteria analysis in writing. When in doubt, classify as fundraising.

5. Supporting Documentation

What they request:

- Time and effort reports for personnel costs

- Facility diagrams showing space allocation

- Invoices and contracts showing service breakdowns

- Samples of joint activity materials

- Board-approved allocation policies

Red flags:

- No time tracking for allocated salaries

- Missing documentation for large allocations

- Retroactive time estimates instead of contemporaneous tracking

Pass the test: Build documentation throughout the year, not at year-end. Use calendars, timesheets, or project management tools to track time allocation in real-time.

6. Treatment of In-Kind Donations

What they verify: In-kind contributions recorded as both revenue AND expense in appropriate functional categories.

Red flags:

- In-kind revenue recorded but no corresponding expense

- In-kind expenses allocated improperly

- No fair market value documentation

Pass the test: When you receive donated goods or services, document the fair value immediately and record both sides of the transaction.

Audit Preparation Checklist

Before your audit, make sure you have:

[ ] Written allocation methodology policy

[ ] Time tracking documentation for allocated personnel

[ ] Facility space measurement documentation

[ ] Copies of all joint activity materials

[ ] Three-criteria test documentation for joint costs

[ ] Year-over-year comparison with variance explanations

[ ] Supporting invoices for major allocated expenses

[ ] Board minutes approving allocation policies

Pro tip: Schedule a pre-audit meeting with your bookkeeper or controller to walk through the functional expense statement together. Identify any questionable allocations and address them before the auditors arrive.

Tips for Analyzing Your Statement

Once your statement is complete, use it strategically:

Compare Against Budget

Are you spending more or less than projected in each functional category? Significant variances should trigger investigation and adjustment.

Review Trends Over Time

Compile statements for multiple years and look for patterns:

- Are program costs growing faster than revenue?

- Is administrative spending creeping up?

- Are fundraising investments generating adequate return?

Evaluate Program Efficiency

If you operate multiple programs, consider creating program-specific functional expense reports. This reveals which programs are most cost-effective and which may need optimization.

Benchmark Against Peers

Compare your functional expense ratios to similar organizations in your sector. While every nonprofit is different, significant outliers may warrant explanation.

Use Alongside Other Statements

Pair the statement of functional expenses with your statement of activities and balance sheet. Together, they provide a complete financial picture.

Common Mistakes to Avoid

Steer clear of these frequent errors:

1. Inconsistent Allocation Methods

Changing how you split shared expenses from year to year makes trend analysis impossible. Document your methods and stick to them.

2. Forgetting In-Kind Contributions

If you receive donated goods or services, record both the revenue and corresponding expense. This ensures your statement reflects the full value of your operations.

3. Using Business Templates

For-profit expense reports don't include functional categories. Always use templates designed specifically for nonprofits.

4. Improper Functional Classification

Be honest about what qualifies as "program" versus "overhead." Misclassifying expenses to inflate program percentages damages credibility when discovered.

5. Skipping Documentation

Always document how you allocated shared expenses. Auditors and grantmakers will ask for your rationale.

How Aplos Handles Functional Expense Reporting

While the template gives you a great starting point, manually building this statement every year is time-consuming. Aplos Fund Accounting Software streamlines the process:

Option 1: Use 990 Tags

Aplos lets you tag transactions with 990 categories as you record them. When it's time to report, simply pull a tag report that automatically organizes expenses by functional category.

Option 2: Use Fund-Based Tracking

Create separate funds for each functional area. Most nonprofits already use funds for individual programs. You can also create a dedicated fundraising fund to track those costs separately.

Both approaches automatically generate the reports you need for Form 990, board meetings, and annual reports. No manual spreadsheet work required.

Ready to automate your reporting? Try Aplos free for 15 days and see how fund accounting simplifies compliance.

Additional Resources & Next Steps

- Download the free Statement of Functional Expenses Template and start tracking your spending by function today.

- Need help with revenue tracking? Check out the Statement of Activities Template.

- Want to see your overall financial position? Grab the Nonprofit Balance Sheet Template.

- Set up clean expense tracking with the Nonprofit Chart of Accounts Template.

- Create a realistic budget with the Nonprofit Budget Template + Guide.

- Explore Aplos Fund Accounting Software for automated reporting and compliance.

- Need expert support? Aplos Bookkeeping Services can handle your financial reporting so you can focus on your mission.

Frequently Asked Questions

Is the statement of functional expenses required for all nonprofits?

It's required if you file Form 990 (organizations with $200,000+ in gross receipts or $500,000+ in assets). Even if not required, many nonprofits prepare it voluntarily to demonstrate accountability.

How often should I prepare this statement?

At minimum, annually for your Form 990 filing. Many organizations review it quarterly to stay on top of spending patterns and make timely adjustments.

What's the difference between natural and functional expense categories?

Natural categories describe the nature of the expense (salary, rent, supplies). Functional categories describe its purpose (program, administrative, fundraising).

How do I allocate shared expenses?

Use a reasonable and consistent method. Common approaches include time allocation for staff, square footage for occupancy costs, and usage metrics for technology. Document your methodology.

Can accounting software generate this automatically?

Yes. Fund accounting software like Aplos can automatically generate functional expense reports using tags or fund structures, saving hours of manual work.

.png)

Make your accounting work for your mission today

Start your 15-day trial today. No credit card required.