.png)

Nonprofit Budget Template: Complete Guide + Free Download

A well-planned nonprofit budget is your roadmap for making mission-driven financial decisions. It helps you allocate resources strategically, demonstrate stewardship to donors and board members, and navigate through both planned growth and unexpected challenges.

Unlike for-profit budgets that focus on profit maximization, nonprofit budgets balance mission impact with financial sustainability. They must account for restricted funding, program-specific expenses, and the unique reporting requirements that come with accepting donor contributions and grant awards.

This guide explains what makes nonprofit budgeting unique, how to build an effective budget, and how to use budget tracking to strengthen your organization. You'll also find a free comprehensive budget template with built-in formulas, charts, and examples across five pre-built worksheets.

Ready to get started? Download the free template now.

Key Takeaways

- Program-first budgeting: Structure your budget around programs and mission delivery, not just expense categories, to demonstrate impact to stakeholders.

- Align with Form 990 categories: Build your budget using functional expense categories (program services, management & general, fundraising) to simplify year-end reporting.

- Plan for restricted funds: Track restricted and unrestricted revenue separately to ensure you spend donor-designated funds appropriately.

- Budget vs actual tracking: Monthly variance analysis helps you spot problems early and make data-driven adjustments throughout the year.

- Build in reserves: Include 3-6 months of operating expenses in your budget as a cash reserve to weather revenue fluctuations and unexpected costs.

- Make it visual: Charts and dashboards help board members and funders quickly understand your financial story without drowning in numbers.

What Is a Nonprofit Budget?

A nonprofit budget is a detailed financial plan that projects your organization's revenue and expenses over a specific period (typically one fiscal year). It serves as your financial roadmap, guiding decisions about:

- Which programs to launch, expand, or scale back

- How many staff members you can afford to hire

- Whether you can take on a new grant that requires matching funds

- How much to invest in fundraising to generate sustainable revenue

- Where to cut costs if donation revenue falls short of projections

Beyond internal planning, your budget is a critical communication tool. Foundations review your budget before awarding grants. Board members rely on budget-to-actual reports to fulfill their fiduciary oversight responsibilities.

Why Nonprofit Budgeting Is Different From For-Profit Budgeting

Nonprofit budgeting has unique characteristics:

Mission over profit: Your budget prioritizes program impact and community benefit rather than profit margins or shareholder returns.

Revenue restrictions: Much of your income may be restricted to specific purposes (program-designated grants, donor-restricted gifts, capital campaign funds). Your budget must track these restrictions and ensure compliant spending.

Functional expense allocation: You must categorize expenses by function (program services, management & general, fundraising) to comply with accounting standards and provide transparency to donors.

Uncertain revenue: Unlike businesses with predictable sales, nonprofits often face volatile income streams dependent on donor behavior, economic conditions, and successful grant applications.

Multiple funding sources: Your budget combines individual donations, foundation grants, government contracts, earned revenue, and event income.

Key Components of a Nonprofit Budget

Revenue Categories

Best practice: Separate restricted from unrestricted revenue in your budget to maintain clear visibility into what funds are available for general operations versus specific purposes.

Expense Categories

Nonprofit expenses fall into two classification systems that work together:

Natural Classification (what you bought):

- Personnel (salaries, payroll taxes, benefits)

- Occupancy (rent, utilities, maintenance)

- Office and administrative

- Professional services

- Program supplies and materials

- Marketing and communications

Functional Classification (why you bought it):

- Program Services: Direct costs of delivering your mission

- Management & General: Costs of overall organizational operations

- Fundraising: Costs of donor cultivation and contribution solicitation

Why both classifications matter: The IRS Form 990 requires functional expense reporting. Organizations following GAAP (specifically ASC 958) must report expenses by both natural and functional classification to provide transparency about how resources are used to deliver mission impact and sustain operations.

Our template includes both classification approaches with automatic calculations.

How to Build Your Nonprofit Budget: Step-by-Step Guide

Step 1: Review Last Year's Actuals

Start by pulling your actual revenue and expenses from the previous year (and ideally, the two years before that). Look for:

- Revenue trends by source (are donations growing or declining?)

- Expense patterns by category

- Seasonal fluctuations (year-end giving is typically higher than other periods)

- One-time items that won't recur

- Spending that ran over or under budget

Historical data grounds your budget in reality rather than wishful thinking.

Step 2: Set Strategic Priorities

Before entering numbers, clarify your mission priorities for the coming year:

- Which existing programs will you maintain, expand, or wind down?

- Are you launching new initiatives?

- What fundraising campaigns are planned?

- Do you need to hire staff or fill vacant positions?

- Are you planning capital improvements or equipment purchases?

Your budget should align with and resource these strategic priorities.

Step 3: Project Revenue Conservatively

Budget revenue using realistic assumptions:

Conservative revenue budgeting prevents the painful mid-year cuts that happen when optimistic projections don't materialize.

Step 4: Budget Personnel Expenses First

Personnel costs are typically the largest budget category for nonprofits. Start here:

- List each position (filled and planned new hires)

- Include full salary, payroll taxes (employer FICA is 7.65% of wages; also budget for FUTA, SUTA, and workers' comp), and benefits

- Factor in planned raises or cost-of-living adjustments

- Account for hiring timeline if positions are currently vacant

- Include temporary staff, interns, or contractors

Don't forget hidden personnel costs:

- Recruitment and onboarding expenses

- Professional development and training

- Workers' compensation insurance

Step 5: Budget Program Expenses

For each program, estimate:

- Program-specific supplies and materials

- Program participant costs (transportation, meals, stipends)

- Program-specific facility costs

- Program-related travel

- Subcontractor or consultant fees

- Program evaluation costs

Align program expense budgets with grant requirements if you have program-restricted funding.

Step 6: Budget Administrative and Fundraising Expenses

Include costs that keep your organization running but aren't directly program-related:

Management & General:

- Rent and utilities (allocated across functions)

- General office supplies

- Technology and software subscriptions

- Insurance (liability, property, D&O)

- Accounting and audit fees

- Legal fees

- Bank and credit card fees

- Board meeting expenses

Fundraising:

- Donor database and fundraising software

- Direct mail campaigns (printing, postage)

- Event expenses (beyond ticket sales)

- Donor recognition and stewardship

- Grant writing support

- Marketing and advertising

Step 7: Calculate Your Bottom Line

Subtract total expenses from total revenue:

Surplus (revenue > expenses): Shows financial strength and the ability to build reserves, invest in growth, or launch new programs.

Balanced budget (revenue = expenses): Common for established nonprofits in steady-state operations.

Deficit (expenses > revenue): Acceptable if you're strategically spending down reserves or using one-time restricted funds, but unsustainable long-term.

Many boards prefer to budget a modest surplus to provide cushion for unexpected expenses or revenue shortfalls.

Step 8: Build in Reserves

Your budget should include a line item for reserve building or reserve allocation. Financial best practices recommend nonprofits maintain 3-6 months of operating expenses in unrestricted reserves.

Calculate your reserve target:

Target Reserve = (Total Annual Operating Expenses ÷ 12) × 4

(Using 4 months as the middle of the 3-6 month range)

If you're below this target, budget surplus revenue to flow into reserves until you reach your goal.

Real World Example: How Valley Youth Services Transformed Their Budgeting

Note: This is a fictional example created for illustrative purposes to demonstrate effective budgeting practices.

Valley Youth Services, a $680,000 youth development nonprofit serving at-risk teens, struggled with budget management for years. Their executive director built annual budgets in a basic spreadsheet, but never tracked actual spending against projections. By May of each year, they discovered they were significantly over budget with no time to course-correct.

The Starting Situation (January 2023):

- Annual budget: $680,000

- Cash reserves: $32,000 (less than 3 weeks of operating expenses)

- No monthly budget review process

- Board received only annual financial reports

- Missed two grant deadlines due to inability to provide detailed budget vs actual reports

What They Did:

Leadership downloaded the nonprofit budget template and made three key changes:

- Implemented monthly tracking: The finance manager began updating the Budget vs Actual worksheet by the 15th of each month, documenting all variances over $2,000 or 15%.

- Established quarterly board reporting: The executive director presented the Charts & Visuals dashboard at every board meeting, making financial discussions visual and accessible.

- Built reserve targets into the budget: They budgeted a $28,000 annual surplus specifically to build reserves toward the recommended 4-month level ($227,000 target).

Results After 18 Months (June 2024):

- Cash reserves grew from $32,000 to $86,000 (1.5 months of expenses)

- Identified a $15,000 payroll tax calculation error in March through monthly variance review—caught it before year-end

- Successfully submitted detailed quarterly reports for two federal grants, unlocking $140,000 in new funding

- Board voted to allocate $100,000 of the new grant funding directly to reserves, accelerating their timeline to reach the 4-month target

- Board finance committee meetings dropped from 90 minutes to 45 minutes due to clear visual reporting

- On track to reach 4-month reserve target by December 2025

The executive director's takeaway: "We finally have control over our finances instead of reacting to crises. The monthly discipline of updating actuals and reviewing variances means we catch small problems before they become catastrophic ones, and we're now positioned to seize opportunities like that federal grant that's fast-tracking our reserve goals."

Budget vs Actual Tracking: Turning Your Budget Into a Management Tool

A budget only provides value if you actually use it throughout the year. Budget vs actual tracking compares your budgeted projections against actual revenue and expenses each month or quarter.

How to Track Budget Variance

Our template includes a dedicated Budget vs Actual sheet that automatically calculates:

Variance in dollars:

Actual Amount − Budgeted Amount = Variance

Variance in percentage:

(Variance ÷ Budgeted Amount) × 100 = Variance %

Status indicators:

- ✓ Over Budget (revenue) or Under Budget (expenses) = Good variance

- ⚠ Under Budget (revenue) or Over Budget (expenses) = Concerning variance

- ○ On Track = Within acceptable range

When to Investigate Variances

Not every variance requires action. Each organization should set thresholds based on budget size and materiality. A common approach:

- Significant variances (both large percentage AND dollar amount) → Investigate immediately

- Moderate variances → Monitor closely

- Minor variances → Normal fluctuation

Consider your organization's size when setting dollar thresholds. What's material for a $100,000 budget differs significantly from a $10 million budget.

Common variance causes:

- Timing differences: Planned expenses haven't occurred yet, or revenue came in later than expected

- One-time events: Unbudgeted expenses (equipment repair) or revenue (unexpected bequest)

- External changes: Economic conditions, donor behavior, or cost increases beyond your control

- Poor assumptions: Budget wasn't based on realistic projections

Monthly Budget Review Process

Establish a routine:

- Close your books by the 10th of each month (recording all prior month transactions)

- Generate budget vs actual report for the month and year-to-date

- Review variances over your threshold and document explanations

- Update forecast if trends indicate you'll miss annual budget targets

- Present findings to leadership and board

- Make course corrections if needed (adjust spending, accelerate fundraising, or revise budget mid-year)

Common Nonprofit Budgeting Mistakes to Avoid

1. Budgeting Revenue You Haven't Secured

Budgeting grant applications that haven't been awarded sets you up for painful mid-year cuts. Only include:

- Confirmed renewals of multi-year grants

- Government contracts already awarded

- Foundation grants where you've received an award letter

Create a separate "pipeline budget" for pending grants so you're ready to scale up if they come through.

2. Forgetting Payroll Taxes and Benefits

Budgeting only base salaries without the additional 30-40% for taxes and benefits dramatically underestimates personnel costs. Always include:

- Employer FICA (7.65% of gross wages)

- Federal and state unemployment taxes

- Workers' compensation insurance

- Health insurance premiums

- Retirement plan contributions

- Other benefits (life insurance, disability, etc.)

3. Not Planning for Cash Flow Timing

Your annual budget might balance, but can you make January payroll if most donations come in December? Create a monthly cash flow projection to identify periods where you'll need to:

- Tap a line of credit

- Draw from reserves temporarily

- Time major expenses strategically

4. Underestimating the Indirect Cost of Fundraising

Fundraising costs more than just the development director's salary and your annual gala. Include:

- Database and donor management software

- Donor research tools

- Thank you letters and recognition gifts

- Board member cultivation expenses

- Grant writing support

- Marketing and awareness campaigns that drive donations

5. Creating an Overly Complex Budget

Your budget should be detailed enough to manage effectively but simple enough to explain clearly to board members. Avoid:

- Too many line items (creates administrative burden)

- Program-level detail that changes frequently

- Expense categories that require complex allocation methodologies

A good rule: If you can't explain a line item clearly and concisely, simplify it.

6. Failing to Budget for Contingencies

Consider including a contingency line item for:

- Unexpected expenses (emergency repairs, unplanned legal fees)

- Cost increases (inflation, utility rate hikes)

- Opportunities that arise mid-year

This builds flexibility into your plan rather than forcing you to cut programs when surprises hit.

7. Not Involving Program Staff in the Budget Process

Program directors understand what their initiatives truly cost and what resources they need to succeed. Budget without their input and you'll either:

- Underfund programs that then underperform

- Overfund programs that don't need the full allocation

Collaborate with program leads during the budget development process.

How to Present Your Budget to the Board

What the Board Needs to See

Board members have fiduciary oversight responsibility. They need:

1. High-level summary:

- Total revenue by major category

- Total expenses by functional category

- Net income/surplus/deficit

- Key financial ratios

2. Visual budget charts:

- Revenue breakdown (pie chart showing source diversity)

- Expense breakdown by program vs overhead (demonstrates mission focus)

- Budget trend over multiple years (shows growth trajectory)

3. Key assumptions:

- Revenue growth projections and their basis

- Major expense drivers

- Risks and mitigation strategies

4. Comparison to prior year:

- What's changing and why

- New programs launching

- Expense increases explained

5. Cash flow considerations:

- Seasonal revenue patterns

- Reserve adequacy

- Any planned use of credit lines

Our template includes a dedicated Charts & Visuals sheet that automatically generates board-ready graphics.

Typical Board Budget Approval Timeline

3-4 months before fiscal year: Staff develops initial budget draft

2-3 months before fiscal year: Board finance committee reviews and provides feedback

1-2 months before fiscal year: Revised budget presented to full board

Before fiscal year starts: Board votes to approve final budget

Most boards review and approve annual budgets in these timeframes relative to the start of the fiscal year (January 1 for calendar-year organizations, July 1 for many nonprofits, or whenever your fiscal year begins).

Tips for Presenting Budget Narratives

- Start with mission impact: "This budget enables us to serve 500 additional families"

- Address concerns proactively: If you're budgeting a deficit, explain why it's strategic

- Highlight sustainability: Show you're building reserves and diversifying revenue

- Make it visual: Use charts more than tables

- Invite questions: Budget presentations should be conversations, not lectures

Nonprofit Budget Example

Our free template includes five interconnected worksheets that work together to provide comprehensive budget planning and tracking:

Inside the Template

1. Instructions Sheet

Your starting point with:

- Step-by-step setup guidance

- Color-coded legend (yellow cells for your input, gray cells for protected formulas)

- Clear disclaimer about appropriate use

- Quick reference to get started in minutes

2. Annual Budget (Input)

Your comprehensive yearly financial plan featuring:

- Organization name and fiscal year fields

- Income section with nonprofit-standard categories:

- Individual donations (4010)

- Corporate donations (4020)

- Foundation grants (4110)

- Government grants (4120)

- Membership dues (4210)

- Program service fees (4220)

- Events and fundraising (4300)

- In-kind donations (4400)

- Investment income (4800)

- Other income (4900)

- Expenses section organized by:

- Personnel costs (salaries, payroll taxes, benefits - 5010, 5020, 5030)

- Operating expenses (organized by natural classification)

- Automatic percentage calculations showing each line item as % of total

- Built-in subtotals and net income calculations

- Cash reserves recommendation (4 months of operating expenses)

All income and expense categories use Chart of Accounts numbering (4000 series for revenue, 5000 series for expenses) that aligns with common nonprofit accounting practices.

3. Monthly Detail (Input)

Break your annual budget into monthly projections:

- All the same income and expense categories from Annual Budget

- 12 month columns (Jan-Dec) for detailed cash flow planning

- Annual Total column that automatically sums across months

- Monthly totals that help you identify seasonal patterns

- Essential for grant reporting that requires monthly breakdowns

- Helps you plan for revenue timing and seasonal expenses

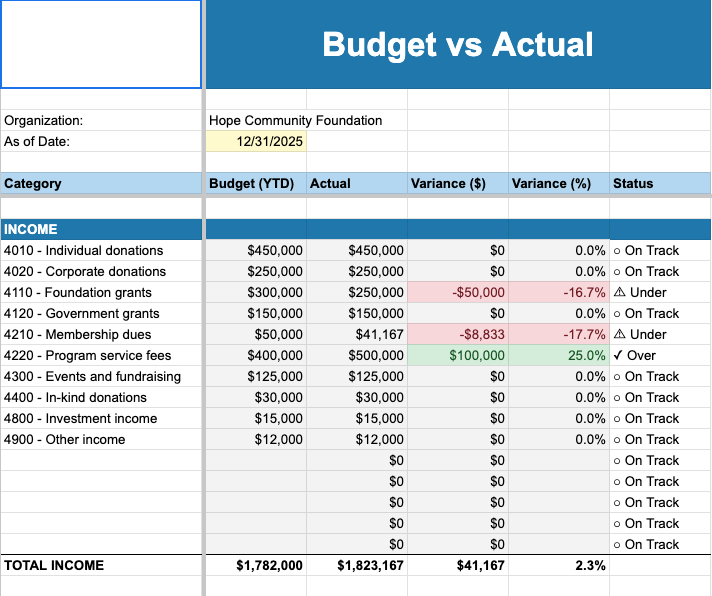

4. Budget vs Actual Tracker

Your variance monitoring command center:

- Budget (YTD) column pulls from your Annual Budget

- Actual column where you enter real results as the year progresses

- Variance ($) automatically calculates the difference

- Variance (%) shows the percentage difference

- Status column with visual indicators:

- ○ On Track (within acceptable range)

- ✓ Favorable variance (over budget revenue, under budget expenses)

- ⚠ Unfavorable variance (under budget revenue, over budget expenses)

- As of Date field to track reporting period

- Separate sections for income and expenses with category-level detail

This sheet transforms your budget from a static plan into an active management tool - update it monthly to spot trends and make proactive decisions.

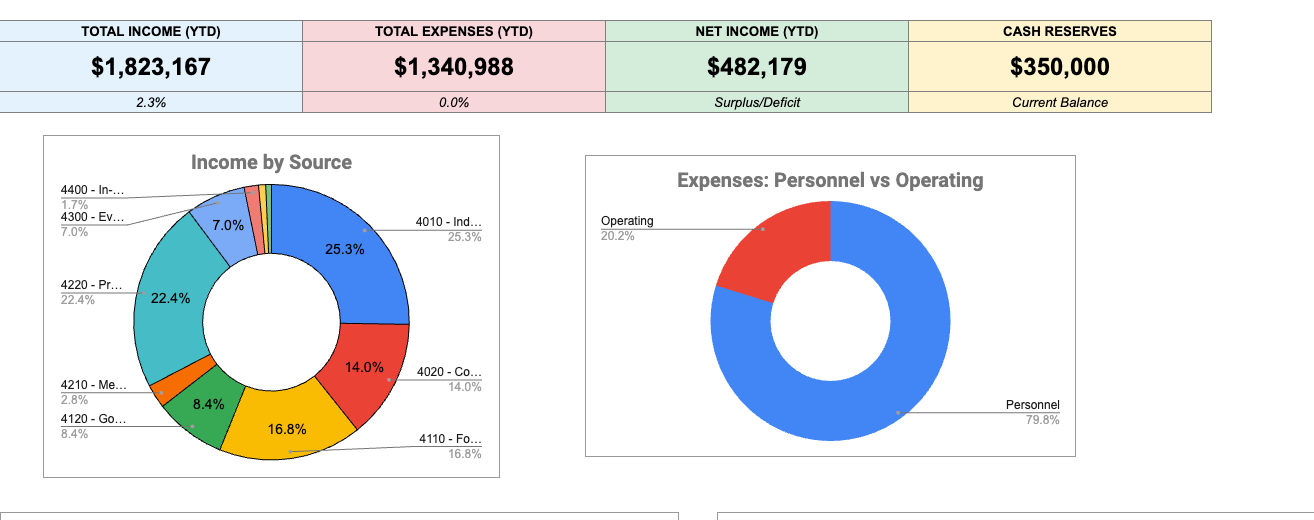

5. Charts & Visuals (Budget Dashboard)

Board-ready visualizations that update automatically:

- Executive summary showing at a glance:

- Total Income (YTD)

- Total Expenses (YTD)

- Net Income (YTD) with Surplus/Deficit indicator

- Cash Reserves with Current Balance

- Income by Source chart (visual breakdown of revenue diversity)

- Expenses: Personnel vs Operating chart (demonstrates spending allocation)

- Monthly Net Income Trend chart (shows financial trajectory over time)

- Net Income vs. Month chart (identifies seasonal patterns)

These visuals help board members and funders grasp your financial story in seconds without reviewing detailed line items.

How the Sheets Work Together

All five worksheets interconnect seamlessly:

- Enter your annual plan in Annual Budget → it flows to Budget vs Actual and Charts & Visuals

- Enter monthly detail in Monthly Detail → validates against your annual totals

- Update actuals in Budget vs Actual → charts automatically refresh to show current performance

- Review Charts & Visuals → see board-ready summaries without additional work

No complex formula work required - just enter your numbers in the yellow input cells and let the template do the calculations.

From Budget Template to Accounting Software

Spreadsheet templates provide an excellent starting point, but many nonprofits eventually outgrow them as complexity increases:

When to Consider Accounting Software

You might benefit from purpose-built nonprofit accounting software if:

- You manage multiple programs with separate budgets

- You track restricted funds that require detailed allocation

- You need real-time budget vs actual reporting

- Multiple staff members need budget access simultaneously

- You want to budget by fund, program, location, or department

- Grant requirements demand specific budget reporting formats

- You're spending too much time on manual budget updates

What Accounting Software Provides

Real-time tracking: See budget vs actual instantly as you record transactions

Multi-dimensional budgeting: Create budgets by program, fund, grant, department, or location without complex spreadsheet workarounds

Automated reports: Generate board-ready budget reports in minutes, not hours

Audit-ready documentation: Maintain clear audit trails for all budget changes and approvals

Integration: Connect budgets directly to your general ledger, eliminating manual data entry

Collaboration: Multiple team members can access and update budgets with permission controls

Aplos fund accounting software includes comprehensive budgeting tools designed specifically for nonprofit needs, with free demos available to see how it compares to spreadsheet-based approaches.

Additional Resources & Next Steps

- Download the free Nonprofit Budget Template with five pre-built worksheets including annual planning, monthly detail, and budget vs actual tracking.

- Track your spending by purpose with the Statement of Functional Expenses Template.

- Understand cash flow timing with the Nonprofit Statement of Cash Flows Template.

- Organize your transactions with the Nonprofit Chart of Accounts Template.

- Create financial statements with the Statement of Activities Template and Nonprofit Balance Sheet

- Explore Aplos Fund Accounting Software for automated nonprofit budgeting and financial management.

- Need expert support? Aplos Bookkeeping Services provides monthly budget vs actual reporting and financial analysis.

- Need to find grants? Check out our Nonprofit Grant Directory on Keela.

Frequently Asked Questions

How much detail should our budget include?

Balance detail with usability. Your budget should be detailed enough to manage effectively but simple enough that board members can grasp key points quickly. The right level of detail depends on your organization's size and complexity.

How often should we review budget vs actual?

Management should review budget vs actual monthly to catch issues early. The board's review schedule can be monthly or quarterly, depending on your organization's size, complexity, and governance requirements. Monthly reviews provide faster course correction, while quarterly reviews reduce administrative burden. The key is establishing a consistent schedule and acting on variances promptly.

What's a healthy reserve level for nonprofits?

A commonly recommended target is 3-6 months of operating expenses in unrestricted reserves, though appropriate reserve levels vary by organization. Consider your funding volatility, revenue diversity, fixed costs, and access to credit when setting your target. Organizations with more unpredictable revenue streams or longer funding cycles may need higher reserves. Calculate a reserve target using: (Annual Operating Expenses ÷ 12) × desired months of coverage.

How do we handle restricted revenue in our budget?

Create separate columns or sections for restricted and unrestricted revenue. Use classes or project codes to track expenses against specific grants. This prevents you from accidentally counting restricted funds as general operating cash and helps demonstrate to donors that their gifts were spent as intended.

Can we change our budget mid-year?

Yes. Budget amendments are common when circumstances change significantly (major grant awarded, unexpected expense, revenue shortfall). Present amended budgets to your board finance committee and full board for approval, and document the reasons for changes.

.png)

Make your accounting work for your mission today

Start your 15-day trial today. No credit card required.